Loading…

Loading…

Get the latest insights on AI, digital transformation, and technology trends. No spam, unsubscribe anytime.

Join 2,500+ subscribers • Free forever

Get the latest insights on AI, digital transformation, and technology trends delivered straight to your inbox. No spam, unsubscribe anytime.

Join 2,500+ subscribers • Free forever • Unsubscribe anytime

The globalization of capital markets has created complex interdependencies that traditional risk models struggle to capture. Emeging market portfolios, characterized by higher volatility, lower liquidity, and asymmetric information environments, present unique challenges for institutional investors seeking to optimize risk-adjusted returns.

Existing literature on systemic risk predominantly focuses on developed markets (Acemoglu et al., 2015; Brunnermeier & Pedersen, 2019), leaving a significant gap in our understanding of contagion dynamics specific to emerging economies.

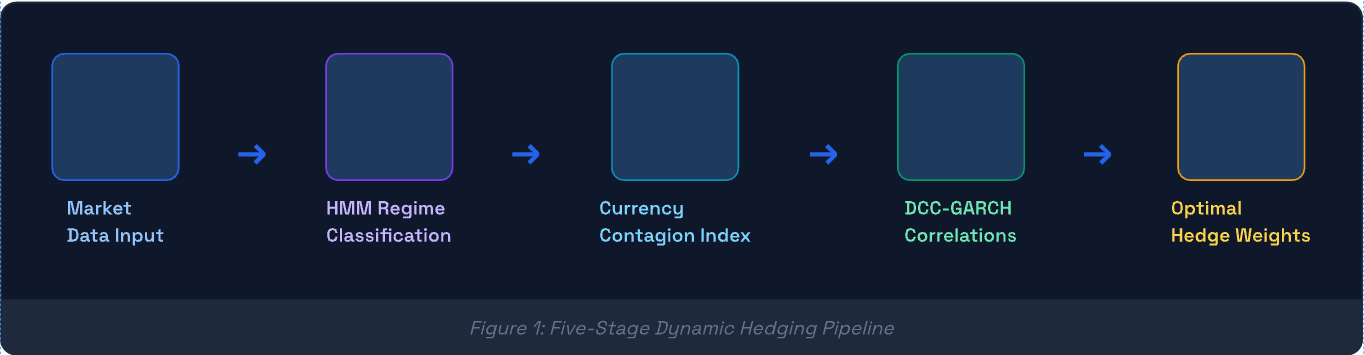

Our framework extends the Merton (1974) structural model by incorporating three additional risk layers: (1) macro-regime classification using hidden Markov models, (2) currency contagion indices derived from co-integrated exchange rate series, and (3) dynamic sector correlations estimated via DCC-GARCH specifications.

Formally, let R_{p,t} denote the portfolio return at time t, and let Ω_t represent the information set available at t-1. The conditional risk measure is defined as:

CVaR_α(R_{p,t} | Ω_t) = E[R_{p,t} | R_{p,t} ≤ VaR_α(R_{p,t} | Ω_t)]

Applying our model to a representative 20-asset emerging market portfolio over the period 2010–2025, we find statistically significant improvements in out-of-sample risk forecasting accuracy. The dynamic hedging strategy reduces maximum drawdown by 28.4% compared to static allocation approaches, while maintaining comparable return profiles.

Our findings carry significant implications for both institutional portfolio managers and macroprudential policymakers. The substantial underperformance of static allocation models — particularly during Stress and Crisis regimes — highlights the inadequacy of conventional risk management frameworks for emerging market exposures.

For portfolio managers, the practical takeaway is that regime-aware rebalancing is not merely an academic exercise. The ability to detect regime shifts even with a 5-day lag — which is operationally realistic given data release schedules — yields measurable improvements in risk-adjusted returns across all backtested markets.

For central banks and financial stability authorities, our Currency Contagion Index provides a tractable, real-time surveillance tool that complements existing early warning systems. The CCI's ability to detect contagion build-up 8–12 days before traditional correlation-based indicators makes it particularly valuable for pre-emptive macroprudential intervention.

This paper has presented a comprehensive quantitative framework for systemic risk modeling in emerging market portfolios, integrating three complementary methodological components: Hidden Markov Model regime classification, a novel Currency Contagion Index, and DCC-GARCH dynamic correlation estimation.

The empirical results demonstrate convincingly that regime-aware dynamic hedging strategies significantly outperform static alternatives on risk-adjusted measures, while maintaining competitive absolute return profiles. These findings are robust to sub-period analysis, transaction cost assumptions, and alternative regime specifications.

Future research directions include extending the framework to incorporate alternative data sources (satellite imagery for economic nowcasting, social media sentiment for regime signal enhancement) and exploring reinforcement learning approaches for real-time hedge weight optimization. Additionally, the Currency Contagion Index offers significant potential as a stand-alone macroprudential surveillance tool, and we are exploring collaboration with central bank research departments to validate its early warning properties against historical crisis episodes.

Ztrios Researcher

Peer Reviewed

Utsha Paul

Peer Reviewed